Fast Growing Compounder and Competitor Exits from Market

50% of Balance Sheet in Cash. FCF >22%. Revenue 20% CAGR.

Key metrics

50% of Balance Sheet is Cash

Revenue 20% CAGR

Competitor withdraws from market

+22% Free Cash Flow

Asset-light

0 Debt

The following company is a SaaS provider with a 20% revenue CAGR in the last 5 years. There is a lot of room to grow as they expand to Asia and other industries. Their software solution is 1 of 2 solutions and the competitor withdraws from the niche market.

The company’s moat is sticky due to switching costs. When fully integrated, it is hard to switch to other solutions. Their industry-specific adjusted software seamlessly integrates into the customer’s workflow. For competitor solutions, customers have to adjust the workflow to the software.

The industry this company operates in is expected to grow up to 13% annually till 2029. The company itself is expected to grow faster!

Enough said, let’s dive in!

The Business

Today’s business is Planisware ($PLNW). A French SaaS provider for multi-specialist project management solutions. The company spun off from Thales (defense industry) in 1996 and IPO’ed in April 2024. The current market cap is €1.4 billion, which gives enough runway to grow multiple times over.

Project management software solutions exist in 6 pillars. Planisware is active in 4 of them:

Product Development & Innovation

Project Controls & Engineering

Project Business Automation

IT Governance & Digital Transformation

In the early days, Planisware distributed the software on disks. In 2019, they made the major decision to pivot (with success) to cloud-based systems to generate recurring revenue.

The company manages and owns the servers themselves, but rents the datacenter space. Planisware owns the entire technical stack to ensure a high level of privacy and security. While the company mainly sells subscriptions, it offers licenses (non-recurring) to industries that require the software to run in-house.

Other forms of recurring revenue come from cross-selling and up-selling. Think about updates and technical support.

The recurring revenue grew from 69% in 2020 to 89% in 2024.

Customers

Planisware offers 2 software solutions: Enterprise and Orchestra. The former addresses sophisticated project processes for companies with over 10.000 employees. While the latter is geared towards fast deployments for medium-sized companies with at least 500 employees.

Planisware’s software has been adopted in a wide range of industries such as life sciences, automotive, manufacturing, utilities, technology, telecommunications and aerospace and defense.

The company listens to the needs of the industries and makes adjustments in the software accordingly. It allows various industries to seamlessly integrate Planisware’s software into their operational workflow. All the while, many competitors offer 1 solution and the industries have to fit their workflow to the solution.

Financials

Since the company IPO’ed recently, long-term trends are not visible in the financial data. In this analysis, we can’t look at expanding margins or other trends. However, there are 4 years worth of financial data and the company appears healthy.

Balance sheet

The balance sheet looks great. Cash & cash equivalents is half the total balance sheet. It is a huge amount of cash they are hoarding.

Further, the company doesn’t hold long-term debt. They don’t hold inventory. Retained earnings rise yearly. It is exactly what you expect from a fast-growing asset-light company.

There is one interesting item on the balance sheet, the contract liabilities, which is deferred revenue. Planisware sells multi-year contracts and in some cases receive the full amount upfront.

The company received the money, but hasn’t done the required work in exchange. Thus, the money is considered a liability. The contract liability is for work due within a year.

Even though it is considered a liability, it increases the working capital. Receiving the revenue upfront functions basically as an interest-free loan.

The growing contract liability is a derivative for orders/contracts. If the number increases yearly, then they have acquired more customers. Or more customers prefer to pay upfront, which benefits Planisware’s cash flow.

Cash flow

The operating cash flow increases mostly due to the net income and working capital increase. The capital expenditures have increased slowly in the last 4 years. In the past years, the company expanded its datacenter and opened office locations.

Due to the low CapEx and increasing operating cash flow, the free cash flow margins are steady above 22% and doubled in 3 years. The company uses the FCF typically to pay off short-term debt and increase dividends.

The financing cash flow tells us that the company increased the outstanding shares a couple of times in the past 5 years. The last issuance was IPO related.

In the past year, they bought back an insignificant amount of shares. Both years equate to approximately €50.000.

The issuance of shares and minimal buy-backs makes it unclear where management stands regarding the outstanding shares. Looking at the cash flows, issuance isn’t needed at all.

Income statement

Planisware’s revenue increased the last 5 years by over 17% per year. The gross profit hovers around 70%. It seems low compared to competitors, but Planisware includes staff costs like salaries, bonuses, pensions and benefits. Also, costs related to hardware maintenance, support and depreciation are added.

Management spends around 13% of revenue on R&D every single year. Operating margins fluctuate between 25-29%.

Low taxes (17%) and 0 interest payments keeps the net income around 24-26%.

Management

Planisware started out with 4 founders who are still active today in various roles. All of them are also on the board of directors. Together they have navigated the company through an ever-changing industry.

Each of the founders has their own specialties in business, project management, engineering, AI and leadership.

Management has shown to think long-term. For example, due to high inflation in the past, they renewed contracts with customers that allow for price increases. They could charge a lot more, but choose not to. The price raises with inflation.

According to management, it isn’t sustainable to increase prices faster than that. They like to think of customers as long-term partners.

Ownership

Planisware is controlled by Olhada. It is the majority shareholder with 63.3% of the shares and voting rights. Olhada is a LLC owned by the founders and their respective families. We can conclude that Planisware is indirectly owner-operated.

A collective shareholding organized by Planisware, holds the employees’ shares. The holding equates to 5% of the shares and is the 2nd largest owner.

The company is heavily owner-operated, and many employees have skin in the game. Ideal for investors.

During the research, it turns out that the investment fund originally founded by the ‘father of growth investing’ T. Rice owns a 2.2% stake in Planisware. A good sign, right?

The investment fund got the chance to buy in at €16 a share at the IPO before the first quote (€21) registered.

Growth

Mordor Intelligence projects that Planisware’s serviceable market will grow 11-13% till 2029. The industry’s growth is mainly driven by the willingness of managers to improve processes, access to resources and manage complexities between departments and location.

It has become clear for enterprises that project management solution from Planisware is an expenditure that reduces costs throughout the company. This realization increases the budget for such software solutions rapidly.

While the market grows fast, Planisware grew faster in the past, 20% CAGR over 5 years. The growth is primarily driven by the increasing market and market spend. Upselling and cross-selling increase what the companies spend when they get locked in. Further, more companies become the size Planisware has viable solutions for.

Planisware started with 22 users in 1996 to over 11,000 users in 2021 at a large pharmaceutical company, as a result of cross-selling to several other departments and segments, adding new functions and extensions on request and upselling product enhancements.

Planisware also penetrate new markets in Asia and the non-IT sector. Lastly, the company has pricing power due to the stickiness (see section Moat). Although the pricing is treated carefully, and mostly adjusts prices for inflation per contract.

Research shows that companies grow faster compared to peers when they are serial acquires. In the project management industry, this is difficult to achieve as the industry hosts a few players. A new acquisition by Planisware isn’t likely.

However, the company made an acquisition in 2018. This became the Orchestra solution targeting smaller companies.

Competitors

According to Gartner’s Adaptive Project Management Quadrant (below), Planisware has competition from Asana, Monday.com, Planview and Smartsheet. The industry report considers the first 4 as leaders.

Garnter’s Adaptive Project management Quadrant, at the courtesy of Planisware.

Planisware, on the other hand, considers Planview its closest competitor as it provides the only other global modern multi-specialist software in this category.

Garnter defines leaders as those who demonstrate and have an understanding of the wide range of customer needs. They engage in the market as thought leaders and help to drive customer success.

All competitors offer solutions to enterprises, while Asana and Monday.com offer plans per seat with a minimum of 2 seats. They target companies of all sizes, don’t own the technical stack and host the software on AWS. You can see why Planisware consider them direct competitors.

At the same time, Planview is actively moving customers to the cloud and retiring on-premise software.

Here, Planisware separates itself from the rest. They have their own vertical integration and offer on-premise software through licenses. Governments and Aerospace and defense are customers in need of in-house solutions. Aerospace and Defense licensing is a small but increasing space.

As said earlier, Planisware also works directly with industries and adapts the solutions to the industry’s needs. The software adapts to the industry’s workflow and not the other way around as with many other competitors.

Moat

The project management software solutions experience a certain sticky moat. Usually, a department within a company tests and pilots various solutions. After a decision is made, the PM software is rolled out company-wide.

Every employee follows some tutorials or receives training to become familiar with the software. It costs the company money and unproductive time to get every employee up and running. Thus, switching solutions is not easily said and done.

The various competitors have different degrees of entanglement with other software solutions. For example, Asana connects with Google Workspace, GitHub, Customer Relations Management (CRM) and other tools.

Planisware is an all-in-one solution for all departments. There is no need for integration with other tools, but it is possible to do so.

Due to industry-specific adjustments in the software, the provided solutions are more intertwined with the operational workflow. Planisware experiences more stickiness.

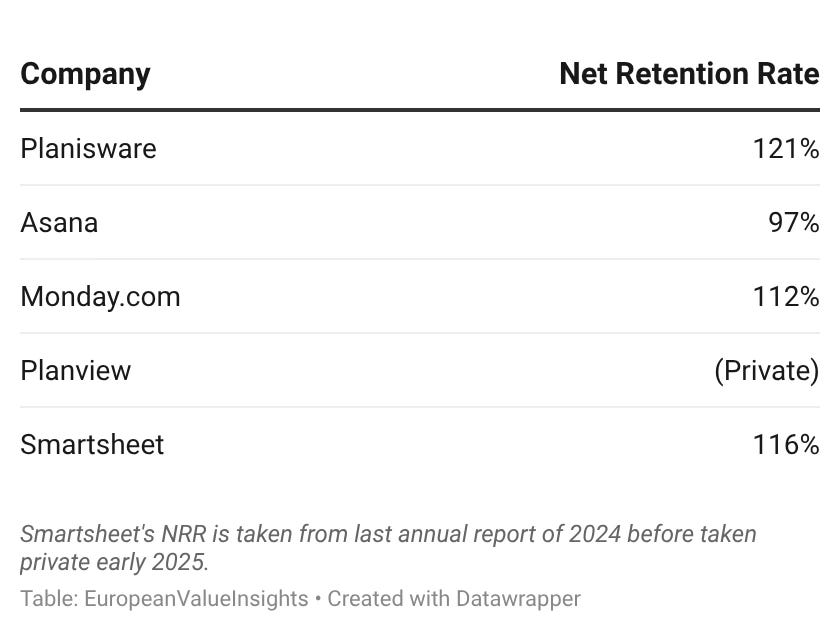

The moat’s strength is somewhat measurable by looking at the industry’s churn rate. The metric indicates the percentage of customers who stop using a product or service during a period.

Planisware reports a below industry average churn rate of just 2%. Competitors don’t report churn rate, but the ‘inverse’ number, net retention rate.

Many customers deciding on Planisware stay around for a while. Anecdotical evidence (reported by Planisware) suggests that many customers expand their internal user base.

Planisware grew from 300 users in 2016 to about 5,000 users in 2022 at a global Aerospace and Defense company, thanks to new configurations, extensions and system migrations implemented across the customer’s entities and departments.

Companies mainly cancel the subscription when they get acquired or when only one department makes use of the smaller version.

Due to technical stack ownership and vertical integration, Planisware experiences a 2nd moat in a niche market. Every competitor moves to the cloud, but Aerospace and Defense and Governments require on-premise solutions. The market is small and viable for 1 player only.

Risks

There is one major risk in the way Planisware operates. They own the technical stack, which makes them responsible for cybersecurity. Servers in Europe, the United States, and Asia store and process project data, business plans and trade secrets on a daily basis.

Currently, Planisware relies on third-party software tools to safeguard its servers and IT systems from cyberattacks and security breaches.

In case third-party software ceases to provide the necessary security, Planisware has to find an alternative or develop the technology in-house.

Another risk is lay-offs. The company states lay-offs don’t have an impact on Planisware as their customers use Planisware to identify places to cut costs. Further, they don’t make explicit statements. Maybe, due to multi-year contracts or other factors, Planisware isn’t directly affected.

What about AI?

The SaaS industry as a whole is being sold off by investors. They feel the threat of AI. Their conviction is that LLMs can create SaaS tools easily. Thus, there is no need for buildings full of programmers anymore.

From personal experience, software development is more difficult than only writing code. It is about design, architecture and innovation.

Vibe coder is a new term used for cohorts who use only LLMs to create programs. They have no background in software development and run in all kinds of problems. Both the vibe coder and the LLM have no idea what they are doing.

Software developers who have a deep understanding of programming can prompt LLMs better. But even then, the LLM isn’t innovative, nor does the code work completely. It blatantly copies existing projects. Most software developers currently use it as an autocomplete tool.

Could more SaaS companies pop up and offer the same solutions? Can’t deny that. However, Planisware adjusts the software solutions to the industry’s needs. They have 30 years more of information and have seen industries develop. Competitors can’t take that away easily.

Cyclicality

The industry itself isn’t cyclical. Expenditures on project management solutions is rising every year. This has to do with the savings for companies and thus a justified expense.

What Planisware noticed in the last year (2025) is delayed contract signatures due to the world’s instability. It creates some cyclicality when the subscription contracts must be renewed.

Revenue and growth are delayed by 1 year. However, it isn’t the typical cyclicality other industries (i.e. automotive) experience.

Valuation

The IPO is just short of 2 years ago and there is not much historical financial data about growth and improvement of margins. The company has reported a 20% CAGR in the past 4 years. The current projected growth is high double digits and later double mid-digits.

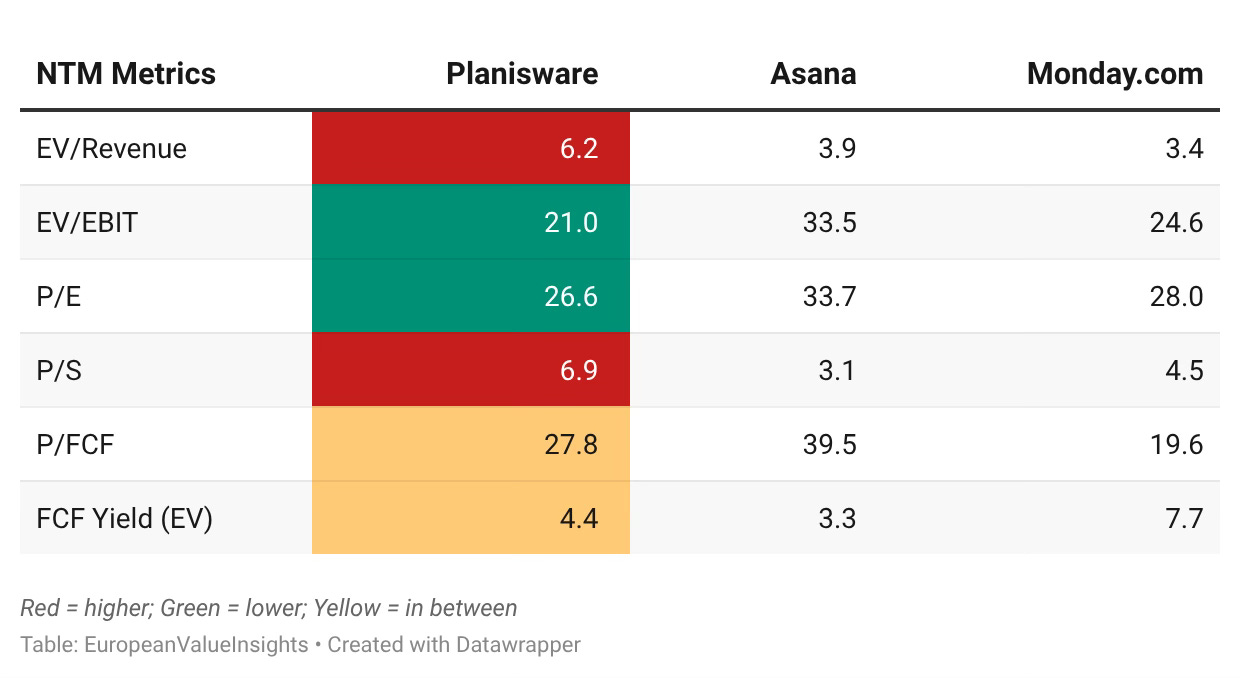

An industry comparison below indicates Planisware’s price to be roughly 1.5 times higher than the competitors. Of course, this assumes that the competitors are fairly priced. Planview and Smartsheet are private companies who lack public data to make this analysis.

Planisware’s revenue is relatively expensive. While the earnings are cheaper compared to the competitors. When we look at the income statements, it becomes clear that Asana and Monday.com spend a lot more on marketing. This shifts the balance from overpaying to underpaying throughout the income statement.

The price paid for FCF is somewhat in between the 2 competitors.

The justification for Planisware’s slightly higher price is:

Offers more specialized software and orientates directly on the needs of certain industries. Competitors offer generic software suitable for all company sizes.

Offers multiyear contracts

Stickier than competitors and have a higher retention rate.

The only one offering on-premise software

Based on this, a share price between 14-15 euros is reasonable. It is lower than institutional investors could buy in during the IPO at €16. But the metrics then come close to Monday.com’s metrics. Since Planisware has the above points, it has a margin of safety built in. From today’s price of 20 euros, this is a 25 to 30 % drop.

A €15 share price lowers the P/E to 20. When growth picks up and investor sentiment too, the share price propels upward faster due to a combination of earnings and P/E increase.

Conclusion

Planisware is a great company that specializes in project management software solutions. It IPO’ed less than 2 years ago and is unusual for me to look at. There is less historical data available.

However, the current balance sheet looks great. Increasing shareholder equity and without any long-term debts.

The company’s moat is expertise and industry-specific solutions. Competitors offer generic solutions. Once the software solutions are integrated, it is difficult to change again, creating a certain stickiness. This is visible in the high retention rate.

All in all, the company is a little overpriced due to the expected growth. The lack of historical margins can’t tell us if the company improves its moat and how quick the return of capital is.

The next annual report will be released at the end of February. Maybe this will shed some light on questions we still have.

For now, a competitor analysis results in a reasonable share price of 14 to 15 euros with margin of safety built in.

Disclaimer

The information provided in this newsletter is for informational purposes only and does not constitute financial, investment, or professional advice. All opinions expressed herein are solely those of the author and are based on publicly available information as of the date of publication. Investments in stocks and other securities involve significant risk, including the potential loss of principal. Past performance is not indicative of future results. Readers are encouraged to do their own research and consult with a qualified financial advisor before making any investment decisions. The author and publisher of this newsletter assume no responsibility for any errors, omissions, or outcomes related to the use of this information.

By reading this newsletter, you acknowledge that the author is not liable for any decisions made based on the content provided.

Some yellow flags: very bad guidance, repeatedly cutting it a lot. Not providing NRR figures amidst these cuts, but they certainly are not getting 120% right now. I want it cheaper

Any Insight on how differentiated the product is vs a Monday.com or other similar software providers?